Dear Students, In this post we have provided Dibrugarh University BCom 6th Sem GST Law and Practice Solved Question Paper 2023. If you want to read the question paper solution scroll down you will get a complete solution which is prepared by our team.

Dibrugarh University B.COM 6th Sem GST Law and Practice 2023

Paper: C-614

COMMERCE (Core)

Full Marks: 80

Pass Marks: 32

Time: 3 hours

(GST Law and Practice)

The figures in the margin indicate full marks for the questions

Question No.1. (a) Fill in the blanks: 1 x 4 = 4

(1) GST is a value-added tax-based tax on consumption of goods and services.

(2) GST number has 15 digits.

(3) The Indian GST model is chosen from the Canadian dual GST country model.

(4) For delayed payment of GST, interest is payable at 18% per annum.

Note: A rate of 24% interest will be applicable in the case when a taxpayer claims an excess input tax credit or makes a reduction in the output tax liability.

(b) Write True or False: 1 x 4 = 4

(1) Input tax credit (ITC) cannot be availed when tax is paid on advance receipt.

Answer: True.

(2) The Union Finance Minister is the Chairperson of the GST Council.

Answer: True.

(3) Filing of GSTR-3B is compulsory for all normal and casual taxpayers, even if there is no business activity.

Answer: True.

(4) The full form of GSTIN is the Goods and Services Taxpayer Inclusion Number.

Answer: False. (Correct: Goods and Services Tax Identification Number)

Question No.2. Write short notes on any four of the following: 4 x 4 = 16

(a) Cascading effect of tax.

Answer: The cascading effect of taxes refers to the situation where taxes imposed at one stage of production or distribution are passed on to subsequent stages, leading to multiple taxation of the same value. For example, when a manufacturer pays a tax on raw materials, this cost is included in the price of the finished product. Then, when a wholesaler purchases the finished product, they pay tax on the inflated price, and the cycle continues until the final consumer pays a price inflated by multiple layers of taxation. This phenomenon can distort pricing, reduce efficiency, and hinder economic growth by increasing the overall cost of goods and services. Governments often seek to minimize this effect through policies such as input tax credits or value-added tax systems.

(b) Deemed supply under GST.

Answer: Deemed supply under GST refers to transactions that are treated as taxable supplies even if no actual sale or transfer of goods or services occurs. These situations typically arise when goods or services are used for non-business purposes or when they are transferred between related parties without consideration. Examples of deemed supplies include:

- Goods or services used for personal use by a business owner.

- Distribution of free samples or gifts by a business.

- Transfer of assets from a taxable to a non-taxable entity, or vice versa, within the same business.

The GST law mandates that tax should be paid on such deemed supplies based on their market value or prescribed valuation rules. This ensures that tax is collected even in scenarios where traditional commercial transactions may not take place.

(c) GST council.

Answer: The GST Council is a constitutional body in India responsible for making recommendations to the Central and State Governments on issues related to goods and services tax (GST). It is chaired by the Union Finance Minister and comprises the Finance Ministers of all the states and union territories. Some key functions of the GST Council include:

- Deciding the tax rates and structure of GST.

- Making recommendations on any changes in GST laws.

- Addressing issues related to tax administration and compliance.

- Resolving disputes arising among states or between states and the Centre regarding GST.

The GST Council plays a crucial role in ensuring uniformity, consistency, and smooth implementation of GST across India, promoting economic integration and simplifying the indirect tax regime.

(d) Dual system of GST.

Answer: The dual system of GST refers to the model where both the central and state governments have the authority to levy and collect taxes on the supply of goods and services within their respective jurisdictions. In India, the dual GST system consists of two components: the Central Goods and Services Tax (CGST) levied by the central government and the State Goods and Services Tax (SGST) levied by the state governments. Both CGST and SGST are levied on the same taxable value of goods and services, ensuring that tax revenues are shared between the central and state governments based on a pre-determined revenue-sharing mechanism. This dual structure allows for a harmonized approach to taxation while preserving the fiscal autonomy of the central and state governments.

(e) Casual taxable person.

Answer: A casual taxable person refers to an individual or business entity that occasionally undertakes taxable supplies of goods or services in a particular state or union territory where they do not have a regular place of business. In the context of GST (Goods and Services Tax), a casual taxable person is required to register under GST if they intend to make taxable supplies in a state or union territory where they are not registered as a regular taxpayer.

Such individuals or entities are required to obtain a temporary GST registration for the duration of their business activities in that state or union territory. The registration process and compliance requirements for casual taxable persons are similar to those for regular taxpayers, including filing GST returns and paying applicable taxes.

The concept of a casual taxable person allows for flexibility in the GST system, enabling individuals or businesses to engage in occasional taxable activities across different regions without the need for a permanent establishment or regular registration.

Question No. 3. (a) What are the basic features of indirect taxes? Mention the list of indirect taxes in the pre-GST regime. 7+7=14

Answer: Basic features of indirect taxes:

- Indirect taxation: These taxes are levied on goods and services rather than directly on individuals or entities.

- Collected by intermediaries: Indirect taxes are typically collected by intermediaries such as producers, manufacturers, or service providers, who then pass on the burden to consumers through the pricing of goods and services.

- Indirect impact: While the tax is paid by the intermediary, its impact is ultimately felt by the end consumer in the form of higher prices.

- Regressive nature: Indirect taxes tend to be regressive, meaning they take a higher proportion of income from low-income earners compared to high-income earners.

- Revenue generation: Governments use indirect taxes as a significant source of revenue to fund public expenditure and provide essential services.

List of indirect taxes in the pre-GST regime:

- Excise Duty: Levied on the manufacture of goods within the country, often on specific goods like alcohol, tobacco, and petroleum products.

- Service Tax: Imposed on specific services rendered by service providers, including telecommunications, banking, insurance, and professional services.

- Value Added Tax (VAT): A state-level tax imposed on the sale of goods, levied at each stage of the production and distribution process, with input tax credits available for taxes paid on inputs.

- Central Sales Tax (CST): Levied on the sale of goods in inter-state trade or commerce by the Central Government.

- Customs Duty: Levied on the import and export of goods, regulating trade and protecting domestic industries.

- Central Excise Duty: An indirect tax levied on the production or manufacture of goods in India.

- Octroi and Entry Tax: Levied by local authorities on the entry of goods into a municipal area for use, consumption, or sale.

These taxes constituted the primary sources of indirect taxation in India before the implementation of the Goods and Services Tax (GST) regime.

Or

(b) Write the evolution of indirect taxation in India. 14

Answer: The evolution of indirect taxation in India can be traced through various phases, reflecting shifts in economic policies and priorities.

Pre-independence era: During British rule, indirect taxes like customs duties, excise duties, and salt tax were prominent, serving primarily as revenue sources for the colonial administration.

Post-independence period: After independence in 1947, India continued with a system of indirect taxes, with the government relying heavily on customs and excise duties for revenue. However, there was a gradual shift towards protectionist policies, leading to high tariffs and import substitution.

Liberalization era: In the early 1990s, India embarked on economic liberalization, dismantling many trade barriers and reducing customs duties. This period also saw the introduction of the Goods and Services Tax (GST) in 2017, unifying various indirect taxes under a single regime, simplifying compliance, and reducing tax cascading.

Current scenario: Today, India’s indirect tax system is primarily governed by GST, which subsumes various central and state taxes such as excise duty, service tax, VAT, and others. GST has streamlined tax administration, improved efficiency, and reduced tax evasion, contributing to economic growth and development.

Overall, the evolution of indirect taxation in India reflects the country’s journey from a colonial economy to a modern, unified tax regime aimed at promoting economic efficiency and growth.

Question No.4.(a) What is Goods and Services Tax (GST)? State the necessary pre-conditions for the levy of Goods and Services Tax (GST) on goods and services. 7+7=14

Answer: Goods and Services Tax (GST) is a comprehensive indirect tax levied on the supply of goods and services in India. It is a value-added tax that aims to streamline the taxation system by replacing multiple indirect taxes levied by the central and state governments.

Necessary pre-conditions for the levy of GST on goods and services include:

- Constitutional Amendment: The Constitution of India had to be amended to empower both the central and state governments to levy and collect GST. This was achieved through the 101st Amendment Act of 2016.

- Agreement between Centre and States: The GST Council, comprising representatives from the central and state governments, was formed to ensure consensus on key aspects of GST, such as tax rates, exemptions, and threshold limits.

- Threshold Limits: A threshold limit was set to determine the turnover below which businesses are exempted from GST registration. Different threshold limits apply for goods and services.

- Harmonization of Tax Rates: The central and state governments had to agree on a common set of tax rates for various goods and services to ensure uniformity across the country.

- Implementation of IT Infrastructure: Robust information technology infrastructure was essential for the smooth implementation of GST, including online registration, return filing, and tax payment.

- Public Awareness and Training: Awareness campaigns and training programs were conducted to educate taxpayers, businesses, and tax authorities about the new GST regime and its compliance requirements.

- Legal Framework: The enactment of necessary legislation, such as the Central Goods and Services Tax (CGST) Act and State Goods and Services Tax (SGST) Act by the central and state governments respectively, provided the legal framework for the implementation of GST.

Or

(b) (1) Define Goods under GST. 7

Answer: As per Section 2 (52) of the GST Act, “Goods” encompasses every kind of movable property other than money and securities. However, it also includes the following:

- Actionable claims: These are rights that can be enforced legally, such as debts or claims.

- Growing crops: Refers to crops that are still attached to the land and are yet to be harvested.

- Grass: Yes, even grass is considered a type of movable property.

- Things attached to or forming part of the land: These are items that are connected to the land but can be severed before supply or under a contract of supply.

Under the Goods and Services Tax (GST) system, goods are classified into different tax slabs based on their nature and usage. Here are some key points about goods under GST:

- Classification: Goods are categorized into different tax slabs ranging from 0% to 28% under GST. The rates are determined based on factors such as essentiality, luxury, and public welfare.

- Tax Rates: The tax rates for goods can vary depending on whether they are classified as essential items (0% to 5%), standard goods (12% to 18%), or luxury items (28%).

- Input Tax Credit (ITC): Businesses can claim input tax credit on the taxes paid on their purchases of goods, which helps in reducing the overall tax burden.

- Compliance: Businesses selling goods under GST are required to maintain proper records, file periodic returns, and adhere to other compliance requirements mandated by the GST law.

- Exemptions: Certain goods such as fresh fruits and vegetables, unprocessed food items, healthcare services, and educational services may be exempted or attract a lower tax rate under GST.

It’s important to consult the latest GST regulations and guidelines for accurate information, as the GST framework and rates may evolve over time.

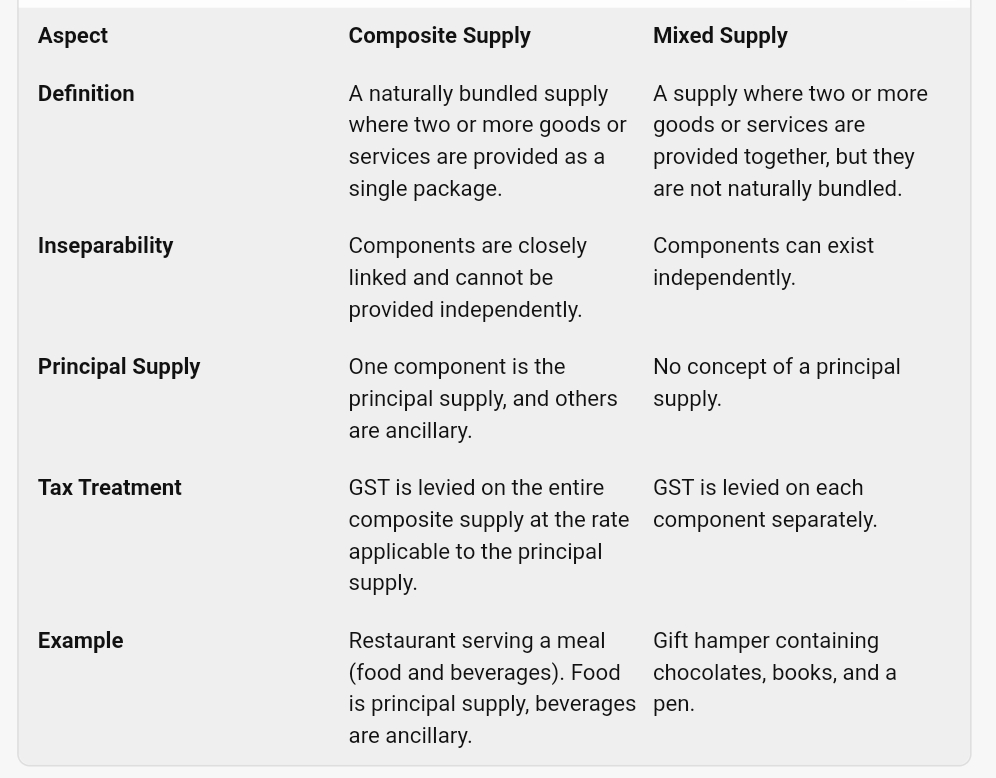

(2) Distinguish between composite supply and mixed supply. 7

Answer:

Question No.5. (a) What is the meaning of the term ‘inspection’? Who can order for carrying out an ‘inspection’ and under what circumstances? When do goods become liable to confiscation under the provisions of the CGST / SGST Act? 4+5+5=14

Answer: Meaning of ‘inspection’: Inspection refers to the act of examining, reviewing, or scrutinizing goods, documents, premises, or records to ensure compliance with applicable laws, regulations, or standards.

Authority to order inspection: Inspections can be ordered by authorized officers under the Central Goods and Services Tax (CGST) Act or the State Goods and Services Tax (SGST) Act. These officers typically include tax authorities, inspectors, or any officer empowered by the respective GST Act.

Circumstances for ordering inspection: Inspections are usually conducted when there is suspicion of tax evasion, non-compliance, or any other irregularity related to GST. They can also be carried out as part of routine enforcement activities.

Goods liable to confiscation: Goods become liable to confiscation under the CGST/SGST Act when they are found to be in contravention of GST laws. This includes cases where goods are smuggled, falsely declared, or where proper GST payments have not been made. Confiscation may also occur if goods are being transported without proper documents or in violation of GST regulations.

Or

(b) What are the safeguards provided in the GST Act in respect of search and seizure? 14

Answer:In the GST Act, safeguards regarding search and seizure include:

- Authorization: Searches can only be conducted by authorized GST officers with proper written authorization.

- Reasonable Grounds: Searches must be based on reasonable grounds to believe that a person has contravened GST laws.

- Recording: The authorized officer must record the reasons for conducting the search and seizure.

- Presence of Witnesses: Witnesses must be present during the search and seizure process.

- Inventory: A list of all seized goods and documents must be prepared and signed by the person from whom they are seized.

- Provisional Release: Provisional release of seized goods can be granted if the person proves that they are not liable to confiscation.

- Time Limit: The seized goods must be released within six months unless circumstances justify further detention.

- Appeal: The person aggrieved by the seizure has the right to appeal to the appropriate authority.

- (a) Explain the mechanism under the CGST Act, 2017 for claiming Input Tax Credit while making payment of taxes. 14

Answer: Under the CGST Act, 2017, the mechanism for claiming Input Tax Credit (ITC) while making payments of taxes involves a structured process to ensure proper utilization of tax credits. Here’s how it typically works:

- Eligibility Criteria: Firstly, a registered taxpayer can claim ITC only if the inputs or input services are used for business purposes and are eligible under the GST law. These inputs could be goods or services used in the course or furtherance of business.

- Receipt of Tax Invoice: To claim ITC, the taxpayer must possess a valid tax invoice or debit note issued by a registered supplier. The invoice should contain the necessary details as prescribed under the GST rules, including the supplier’s GST identification number, recipient’s GSTIN, description of goods or services, tax charged, etc.

- Filing of GST Returns: The taxpayer must file their GST returns accurately and on time, including details of inward and outward supplies. The ITC claim is reconciled with the information submitted by the supplier in their GST returns.

- Verification and Matching: The GSTN (Goods and Services Tax Network) verifies the details provided by both the supplier and recipient to ensure accuracy and prevent fraud. Any discrepancy or mismatch in the details may lead to a delay or rejection of ITC claim.

- Utilization of ITC: Once the ITC claim is approved, the taxpayer can utilize the credit to offset their GST liability while making payment of taxes. The ITC can be utilized towards payment of CGST, SGST, IGST, or cess, depending on the nature of the transaction and the tax jurisdiction.

- Carry Forward and Refund: If the ITC claimed exceeds the tax liability, the excess credit can be carried forward to subsequent tax periods. Alternatively, if there is an excess credit and no immediate use, the taxpayer may opt for a refund as per the provisions of the GST law.

Overall, the mechanism under the CGST Act, 2017, for claiming ITC while making payment of taxes ensures transparency, accuracy, and compliance with GST regulations, thereby facilitating seamless credit flow within the GST system.

Also Read: Dibrugarh University BCom 6th Sem GST Law and Practice Solved Question Paper 2022

Or

(b) (i) Who is required to file an Annual Return under the CGST Act, 2017? 4

Answer: Under the Central Goods and Services Tax (CGST) Act, 2017, the Annual Return is a comprehensive document that taxpayers registered under the Act need to file. It serves as a summarization of the taxpayer’s activities for the entire financial year. The following entities are required to file the Annual Return:

- Regular Taxpayers: Any individual, company, partnership firm, or any other entity registered under the CGST Act, 2017, and engaged in the supply of goods or services or both must file the Annual Return.

- Composition Dealers: Taxpayers registered under the composition scheme are also required to file the Annual Return. The composition scheme is an option available for small taxpayers to pay tax at a fixed rate based on their turnover without the requirement to maintain detailed records.

- Input Service Distributors (ISD): Businesses that are classified as Input Service Distributors, i.e., those entities that receive invoices for input services and distribute the input tax credit to other registered persons, need to file the Annual Return.

- Non-Resident Taxable Persons: Non-resident taxable persons, who are individuals or entities located outside India but are liable to pay tax on supplies made by them in India, are required to file the Annual Return as well.

- Persons liable to deduct TDS (Tax Deducted at Source): Individuals or entities who are required to deduct tax at source under the CGST Act, 2017, also have the obligation to file the Annual Return.

- Casual Taxable Persons: Persons who occasionally undertake transactions involving the supply of goods or services or both in a taxable territory where they do not have a fixed place of business are categorized as casual taxable persons and are required to file the Annual Return.

Failure to file the Annual Return within the prescribed time may attract penalties and consequences as specified under the CGST Act, 2017. Therefore, it’s crucial for all eligible entities to ensure compliance with this requirement to avoid any legal repercussions.

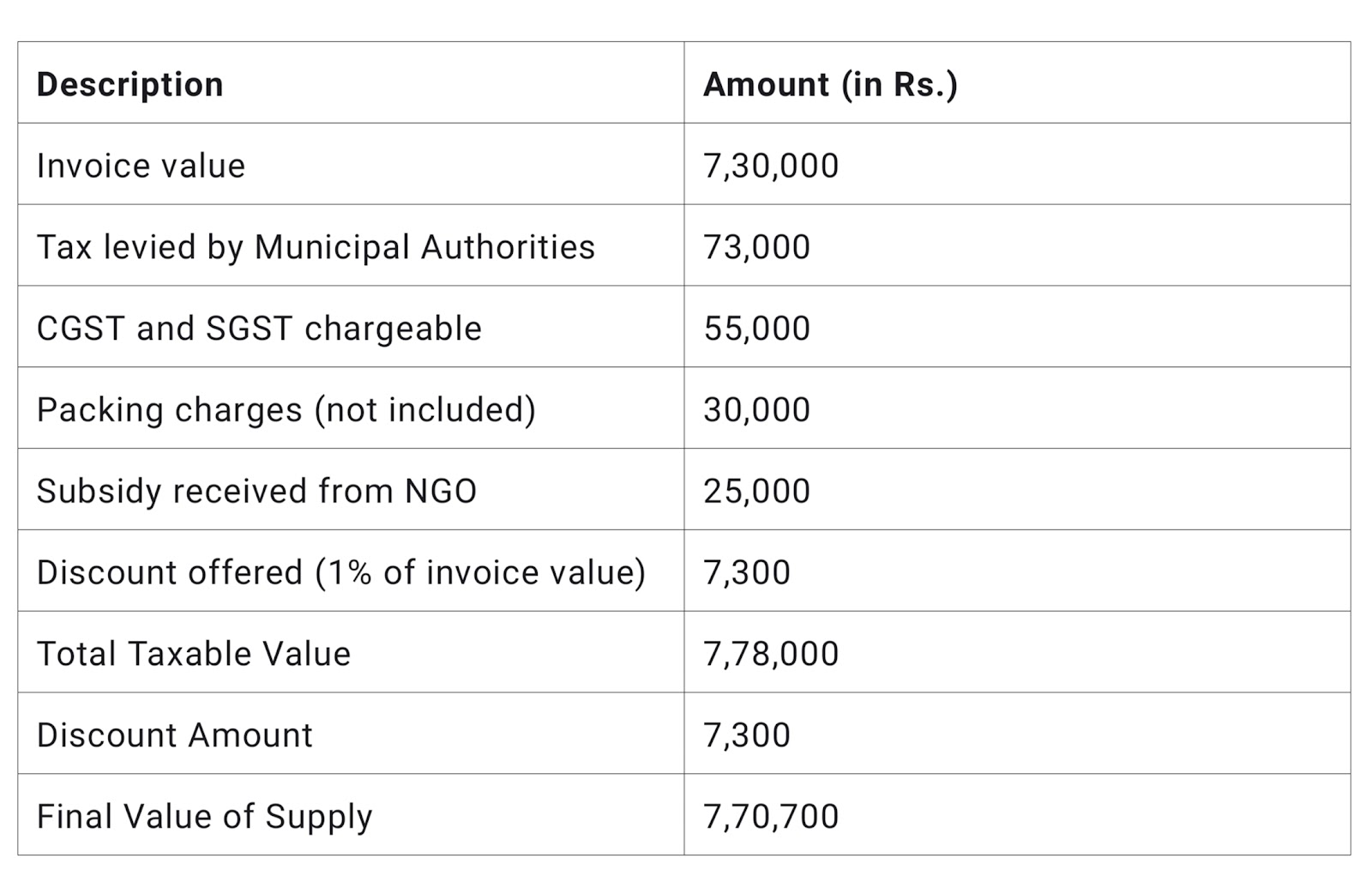

(ii) Haloi Enterprises had made supplies of Rs. 7,30,000 to Deke Enterprises. Municipal Authorities of Dibrugarh on such supplies levied the tax @ 10% of Rs. 73,000. CGST and SGST chargeable on the supply was Rs. 55,000. Packing charges not included in the price of Rs. 7,30,000 amounted to Rs. 30,000. A subsidy of Rs. 25,000 was received from an NGO on the sale of such goods and the price of Rs. 7,30,000 is after taking into account the amount of subsidy so received. The discount offered is @ 1% which was mentioned on the invoice. Determine the value of supply. 10

Answer:

Therefore, the value of supply after considering the subsidy and discount is Rs. 7,70,700.

-000000-

Last Words

We hope you find this question paper solution helpful for your upcoming exam preparation. Please note that the Dibrugarh University BCom 6th Sem Auditing Solved Question Paper 2023, prepared by The Treasure Notes, can be used as reference study material for your studies.